You’ve got a CRM. It works great for managing your wealth management clients. So why isn’t it cutting it for your retirement plan business? You might be thinking it’s you, that you’re not using it right. But the truth is, it’s not you—it’s the tool. Wealth management CRMs, while excellent for their intended purpose, are fundamentally different from what’s needed to manage the complexities of a retirement plan practice.

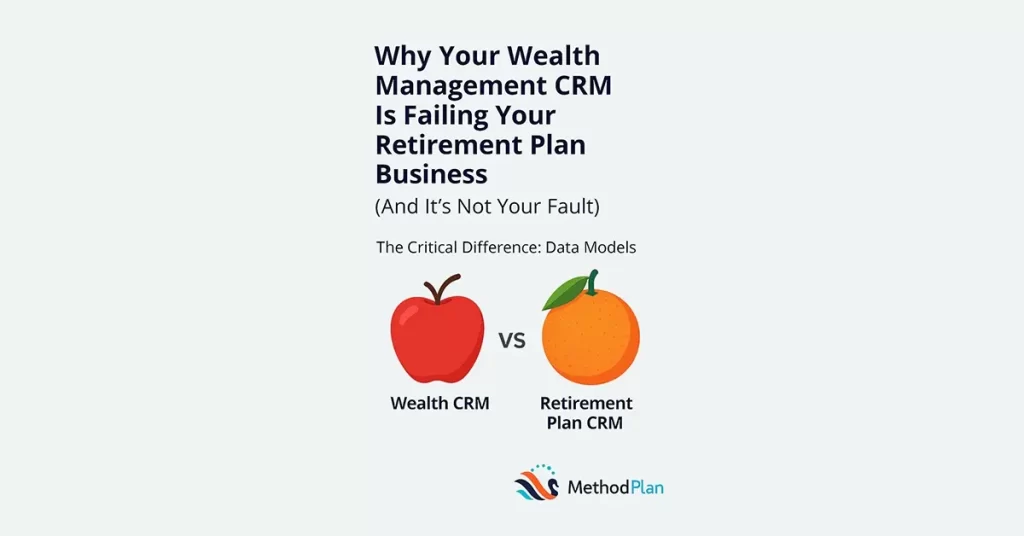

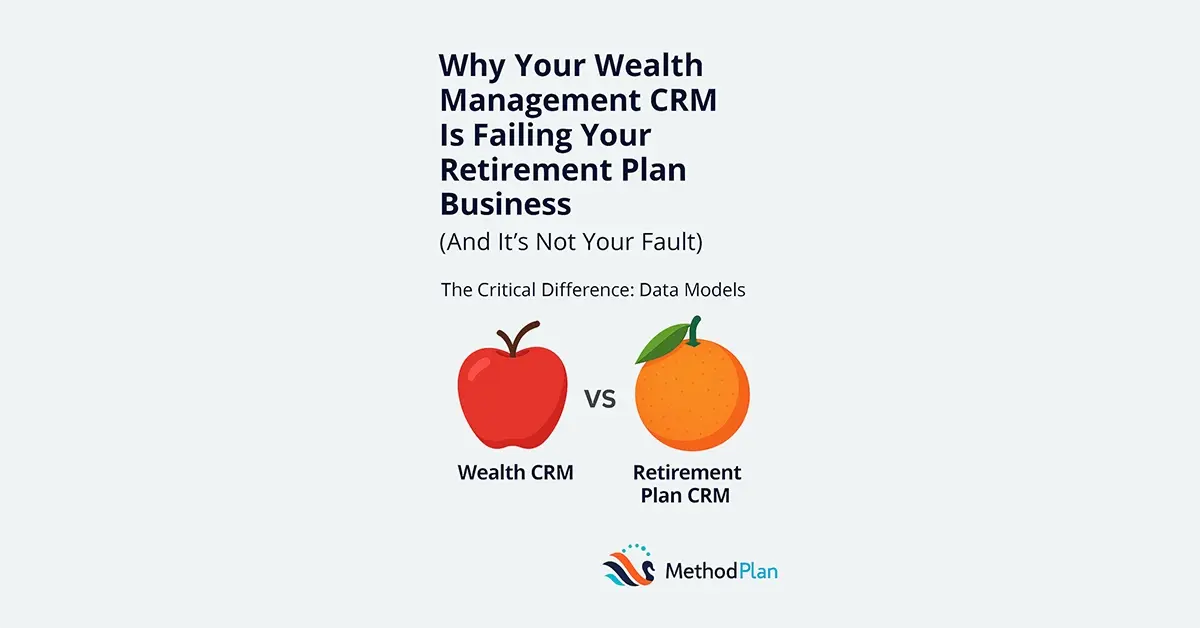

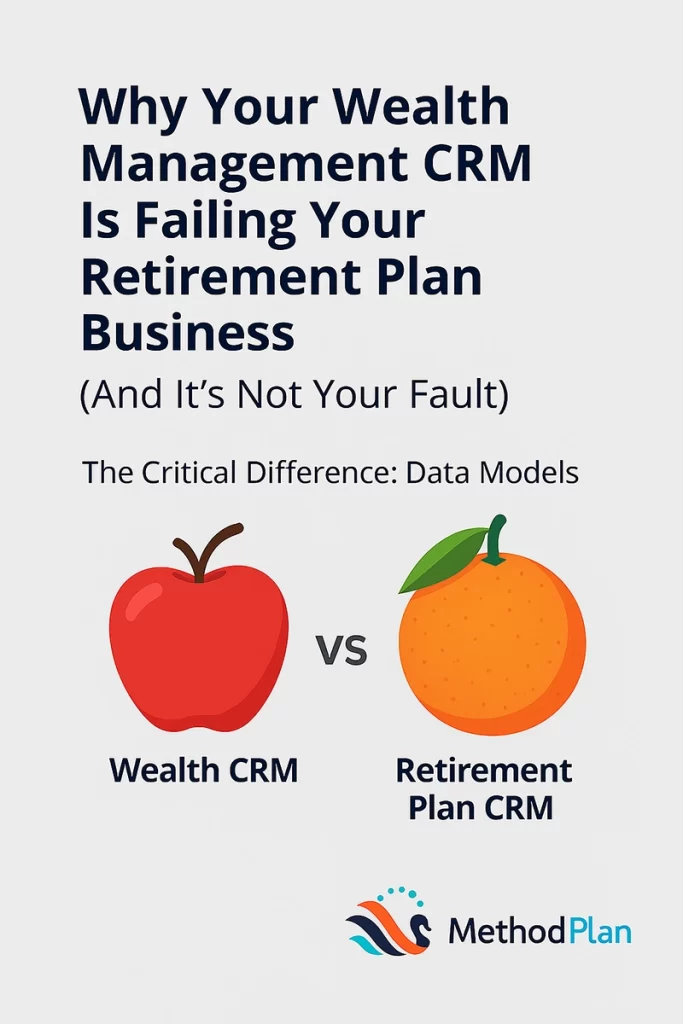

The Critical Difference: Data Models

Think of it this way:

- Wealth Management CRM: Focuses on “John Smith’s portfolio.”

- Retirement Plan CRM: Focuses on “The ABC Company 401(k) Plan.”

A wealth management CRM is designed around the individual client (B2C). It focuses on personal financial details, investment portfolios, and family relationships. It’s built to track individual assets, goals, and interactions.

Retirement plan management, however, operates on a B2B model. You’re dealing with plan sponsors, plan participants, recordkeepers, TPAs, and a multitude of plan-specific details. The data points are vastly different. You need to track plan designs, fee structures, compliance requirements, enrollment dates, and a complex web of relationships between various entities.

Wealth CRMs Are Great—Just Not for This

Let’s be clear: Wealth management CRMs are excellent for what they’re designed to do. They’re powerful tools for managing individual client relationships and portfolios. But they’re simply not built to handle the intricacies of a retirement plan business.

That’s why we created MethodPlan.

Contact us and discover the difference of a purpose-built solution.